B-F-B-ic international Ltd.co , https://www.ledgather.com After the Spring Festival in 2013, the plate market oscillated. According to the market monitoring of Lange Steel Information Research Center, as of March 28, the average price of 20mm middle plate in domestic key cities was 3860 yuan (ton price, the same below), and the average price fell by 5 yuan from the end of last month. The market price of 邯郸20mm plate (represented by Handan Iron and Steel Co., Ltd.) was 3,680 yuan, which was basically 120 yuan lower than that at the end of February. The market price of Shanghai 20mm plate (represented by Maanshan Iron & Steel Co., Ltd.) is 4,000 yuan, a drop of 70 yuan from the end of February. As seen from the chart below, after a sustained decline in the second half of February 2013 and the first half of March, market prices have basically entered the consolidation cycle of weaker shocks since the second half of March.

After the Spring Festival in 2013, the plate market oscillated. According to the market monitoring of Lange Steel Information Research Center, as of March 28, the average price of 20mm middle plate in domestic key cities was 3860 yuan (ton price, the same below), and the average price fell by 5 yuan from the end of last month. The market price of 邯郸20mm plate (represented by Handan Iron and Steel Co., Ltd.) was 3,680 yuan, which was basically 120 yuan lower than that at the end of February. The market price of Shanghai 20mm plate (represented by Maanshan Iron & Steel Co., Ltd.) is 4,000 yuan, a drop of 70 yuan from the end of February. As seen from the chart below, after a sustained decline in the second half of February 2013 and the first half of March, market prices have basically entered the consolidation cycle of weaker shocks since the second half of March.

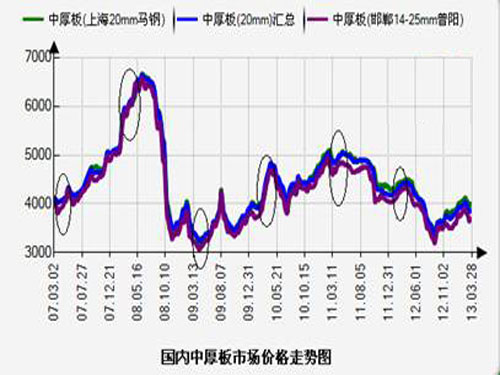

In the past six years, the change in plate price in the plate market can be said to fully reflect the decline of the industry in the steel industry. From 2007 to the first half of 2008, the plate market completed a historic mission of a great revival, with market prices soaring from nearly 4,000 yuan to as high as 6,300 yuan. After the bustling period, the market price of the plate fell rapidly. In the second half of April 2008, the market price of the plate fell to a historical low in five years. In the following four years, the price was basically fluctuating below 5,000 yuan (see details) figure 2). Looking at the market price trend in the March-April period of 6 years in a row, 4 of these are sustained increases, and 2 of them are bottoming out in early April. According to this law, the probability of market rebound in April this year Still larger. Moreover, judging from the price level of the medium and heavy plate market for six consecutive years from March to March, the prices in March-April this year have only been higher than the prices in the economic crisis in 2009, and this year's domestic economic situation is obviously better than in 2009, showing the current market. The bottom price support is already strong. Therefore, judging from the pattern of market price movements over the past 3-4 months, the 2013 plate prices are expected to bottom in early April.

In early 2013, due to the lack of optimism in the production and sales of downstream industries, the overall demand for the plate market was difficult to increase. Construction Machinery: According to the China Industry Research Network, total sales in January and February were relatively low, among which 11058 were digging machine sales, which was 46% lower than the same period of last year. Loader sales were 16874 units, 32% lower than the same period of last year. Bulldozer sales were 747 units. Compared with the same period last year, it dropped 48%. The sales data of construction machinery should be lower than expected, and it is expected that sales of construction machinery will continue to decline year-on-year in March-April.

Shipbuilding industry: In February 2013, the global new ship order was 88 1.944 million CGT, which continued to increase slightly from the previous quarter. Since December of last year, global new ship orders have been growing at a sequential rate in March. Among them, China's handheld orders amounted to 1,827, 33,344,000 CGT, still ranking first in the world; Korea's orders for orders were 777, 28.347 million CGT, a slight increase from the previous month's 775 2825.1CGT.

In January-February, China completed 5.69 million dwt of shipbuilding, a year-on-year decrease of 20.9%; and orders for new vessels amounted to 5.03 million dwt, an increase of 1.9% year-on-year. As of the end of February, the number of handheld ship orders was 106.29 million dwt, a year-on-year decrease of 27.4%. The China Shipbuilding Industry Association released its monthly analysis report on March 22, saying that in the January-February period of this year, the number of new orders received by the Chinese shipbuilding industry increased slightly year-on-year, but the shipbuilding completion volume dropped drastically, and the total industrial output value fell for the first time since the financial crisis. Exports accelerated to decline, and the production and operation situation became more severe.

At the beginning of the year, domestic plate stocks were high, but then inventory slowed down, and market supply pressure gradually eased. According to incomplete statistics from Lange Steel, as of March 22, the domestic plate stocks in 29 key cities in China reached 1.668 million tons, up 2.43% month-on-month, 29.98% year-on-year, and 2.14% year-over-year (see details image 3). In March, the market demand started slowly, and the steel mills shipped relatively normal, there is no large-scale production reduction, maintenance, so the decline in social stocks is still relatively slow, but among them the willingness of traders to lock down orders significantly reduced market inventory consumption has played Must be positive.

In addition, the ex-factory prices of the domestic plate producers have recently been declining, and the cost support for the plate market price has been weakening. Among the first-line steelmakers, Shougang and Baotou Steel maintain stability, Anshan Iron and Steel, and Hegang have both experienced significant declines. From the perspective of second-tier steel mills, the price of Puyang, Wenfeng, Xicheng, Handan Iron and Steel and many other steel mills has declined significantly. Under the low lock price of Puyang Steel Works, there was no significant increase in orders. All indications indicate that there is still a narrow downside for the plate in the short term. (See Table 1 for details)

Based on the analysis of the various factors mentioned above, the entire supply and demand side of the market is still relatively inconsistent, and the market will maintain its inventory in the last two weeks or so and restore demand. With the increase in bottom support for market prices and improved resource liquidity, the plate market price is expected to usher in a reversal opportunity in the second half of April.