In February, the steel demand in the domestic market was not strong. Due to the rapid growth of steel production, the contradiction between supply and demand was further aggravated, and steel prices continued to fall. With the warmer weather, the market demand situation in the later period will have improved, but overall it is difficult to significantly improve, steel prices can hardly rise sharply. Wooden Gate Hinges,Best Hinges For Heavy Wood Gate,5 Bar Gate Hinges,Heavy Duty Wood Gate Hinges Jiaxing Gates Hardware Products Co.,Ltd , https://www.jxgateshardware.com

1. Steel prices in the domestic market continued to fall At the end of February, the comprehensive price index of the CSPI steel products of the Iron and Steel Institute was 96.46 points, 1.19 points lower than the previous period, a decrease of 1.22%, which was 0.28 percentage points less than the previous month, and fell for the sixth consecutive month; 14.66 points, a decrease of 13.19%.

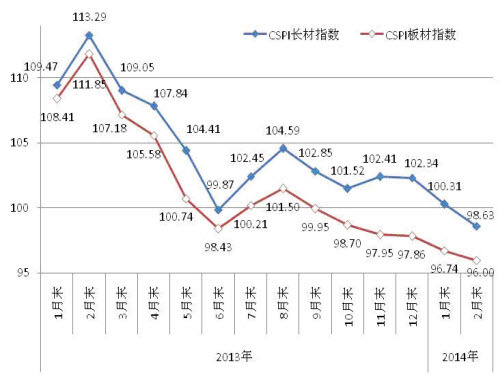

1. Longer-than-plate price declines for long products. At the end of February, the CSPI longevity index was 98.63 points, 1.68 points lower than the previous period, a decrease of 1.67%; the sheet metal index was 96.00 points, a decrease of 0.74 points, or a decrease of 0.76%. The long product price drop is 0.91 percentage points higher than that of the plate. Compared with the same period of last year, the long products index decreased by 14.66 points, a decrease of 12.94%; sheet metal index decreased by 15.85 points, a decrease of 14.17%.

2. Prices of major steel products continued to fall At the end of February, the eight major steel products monitored by the China Iron and Steel Association continued to decline. Excluding cold-rolled steel sheets and hot-rolled seamless tubes, price declines all narrowed from last month. Among them, the prices of high-line and rebar fell by RMB 58/ton and RMB 78/ton, respectively; the decline was relatively large; the price of angle iron fell slightly by RMB 8/ton; plate, hot rolled coil, cold rolled sheet, galvanized Plate and seamless steel pipe prices fell by 11 yuan/ton, 24 yuan/ton, 31 yuan/ton, 5 yuan/ton and 49 yuan/ton respectively.

3, steel prices showed a low level of wave momentum from the situation in each week, the steel prices in February continued to show a slight downward trend week by week. In the second week of March, the CSPI steel price index has dropped for 11 consecutive weeks.

Second, the domestic market analysis of steel price changes in February, the steel market is still in the demand off-season, affected by the rapid growth of iron and steel production, market supply and demand situation is more evident. At the same time, the price of raw materials fell sharply and the supporting effect on steel prices was further weakened.

1. The growth rate of the steel industry slows down, and the demand in the steel market is not strong According to the data from the National Bureau of Statistics, the national fixed asset investment (excluding rural households) increased by 17.9% year-on-year from January to February, which was a 3.3% decrease from the growth rate in the same period of last year. The total investment for the construction project plan increased by 16.8% year-on-year, 2.0 percentage points lower than the growth rate of the same period of the previous year; the industrial added value above designated size increased by 8.6% year-on-year, 1.3 percentage points lower than the growth rate of the same period of the previous year; in February, the Chinese manufacturing PMI It was 50.2%, down 0.3 percentage points from the previous month and falling for the third consecutive month. Among them, the new orders index fell by 0.4 percentage points month-on-month; PPI decreased by 2.0% year-on-year, negative growth for 24 consecutive months, a decrease of 0.2% from the previous month; from the perspective of money supply, the balance of ***** increased by 14.2% at the end of February, respectively. At the end of the month, it was 0.1 and 0.8 percentage points lower than the same period of last year. The net cash withdrawal from the entire month was 1.42 trillion yuan. *** Newly added ** was only 644.5 billion yuan, down 51.2% from the previous quarter. Looking at the overall situation, the growth of the downstream steel industry slowed down in February, and the demand for the steel market was weak.

2. The production of crude steel kept growing, and the contradiction between supply and demand in the market was further aggravated. According to the data of the National Bureau of Statistics, the total pig iron, crude steel and steel (including duplicating timber) in the country in January-February totaled 116.72 million tons, 13.80 million tons and 16573 respectively. Ten thousand tons, respectively, year-on-year increase of 0.2%, 1.7% and 4.9%; average daily output of 2.217 million tons of crude steel, compared with 2.011 million tons in December of last year, a substantial increase of 206,000 tons, an increase of 10.2%. According to customs statistics, in January-February, China exported 11.57 million tons of steel, an increase of 2.41 million tons, an increase of 26.3%; 2.34 million tons of imported steel, an increase of 340,000 tons, an increase of 16.8%; equivalent to a net export of crude steel 982 Ten thousand tons, an increase of 2.2 million tons, an increase of 28.87%. Based on the above data, the average daily supply of crude steel in the domestic market during January-February was 2.05 million tons, an increase of 9.6% over the previous year. In the off-season demand for steel, the supply of steel resources has continued to increase substantially, and the situation of oversupply of the market has intensified.

3. The decrease in the price of raw materials such as iron ore increased, and the supporting effect on steel prices weakened. In February, the prices of raw materials for steel production continued to decline, and the decline was greater than last month. Of which: domestic iron concentrates and imported iron ore prices fell 27 yuan / ton and 50 yuan / ton, respectively, decreased by 2.77% and 5.56%, respectively, 0.76 and 3.39 percentage points increase over the previous month; coking coal and metallurgical coke The price dropped by RMB 80/ton and RMB 110/ton, respectively, a drop of 7.34% and 8.45%, respectively, which was an increase of 0.11 and 2.87 percentage points from the previous month; the price of scrap fell by RMB 24/ton, a decrease of 1.00%. The price of iron ore and coal coke dropped sharply, and the supporting effect on steel prices further weakened.

3. In the international market, the price of steel continued to decline. At the end of February, CRU International's comprehensive steel price index stood at 164.9 points, a decrease of 3.4 points from the previous quarter, a decrease of 2.0%, an increase of 1.9 percentage points from the previous month, and a decrease of 16.2 points from the same period of the previous year. The decrease was 8.9%.

1. The price of long products and sheets continued to drop at the end of 2. The CRU long products price index was 179.8, a decrease of 4.4 points from the previous month, a decrease of 2.4%, an increase of 1.8 percentage points from the previous month; the price index of sheet metal was 158.2 points, a decrease of 2.7 points from the previous month. The decrease was 1.7%, an increase of 1.6 percentage points from the previous month. Compared with the same period of last year, the long products index decreased by 22.4 points, a decrease of 11.1%; sheet metal index decreased by 12.5 points, a drop of 7.3%. 2. Steel prices in North America and Europe rose from rising to falling, and Asia continued to decline. (1) North American market At the end of February, the CRU North American steel price index was 174.6 points, a decrease of 5.3 points or 2.9% from the previous quarter. In February, the U.S. manufacturing PMI was 53.2%, up 1.9 percentage points month-on-month. Among them, the production index dropped sharply by 6.6 percentage points, the inventory index rose sharply by 8.5 percentage points, and the new orders index rose by only 3.3 percentage points, indicating that demand growth mainly depends on inventory growth; at the end of February, the US crude steel capacity utilization rate was 77.4%. , 0.9% lower than the same period of last year. The price of sheet metal in the U.S. market dropped significantly this month, and the decline in long products prices was relatively small.

(2) European market At the end of February, the CRU European steel price index was 156.5 points, down 3.8 points month-on-month, or 2.4%. In February, the eurozone manufacturing PMI index was 53.2%, a decrease of 0.8 percentage points from the previous quarter. Among the major countries in the euro area, German and Italian manufacturing PMIs were 54.8% and 52.3% respectively, down 1.7 and 0.9 percentage points respectively; the French manufacturing PMI rose to 49.7%, still below 50%. The prices of steel bars, small sections, wire rods, and cold rolled coils in the German market this month rose from low to high. The prices of steel and medium plate prices remained stable. The prices of hot rolled coils and hot dip galvanized sheets continued to rise, but the increase narrowed.

(3) Asian markets At the end of February, the CRU Asian steel price index was 165.0 points, a decrease of 2.5 points from the previous month, a decrease of 1.5%. In February, Japan's manufacturing PMI new export orders index fell to 55.5%, down 1.1% from the previous quarter. Its new export order index fell by 1.3 percentage points; China's manufacturing PMI was 50.2%, down 0.3 percentage points month-on-month, of which the new orders index fell to 50.5%, down 0.4 percentage points; the Korean manufacturing PMI fell to 49.8%, the chain Declined by 1.1 percentage points, its new export orders index fell by 1.3 percentage points. The price of steel bars and wire rods in the Far East market rose from high to low this month, small sections and related prices remained stable, and prices of medium plate and thin plate steel rose slightly, but the decline rate narrowed.

Fourth, the analysis of the price trend of the later steel market With the warming of the weather, the steel demand in the domestic market will gradually start. As the economic development still has downward pressure, the growth of steel demand also shows a slowing trend. As the market oversupply situation is still difficult to reverse in the short term, steel prices in the market will gradually stabilize in the later period, but it will be difficult to recover sharply.

1. The national economy maintains a relatively rapid development, and the demand for steel products keeps growing In the “***†government work report, China’s GDP growth target this year is set at around 7.5%, slightly lower than the growth rate of the previous year. In order to maintain stable and rapid economic development, the country will continue to implement a proactive fiscal policy and a prudent monetary policy. The entire society's fixed asset investment is expected to grow by 17.5%, which is still a relatively rapid growth. The projected target for the value-added of industries above designated size is around 9.5%. Slightly below the level of the previous year. As a key factor for steady growth, urbanization is a powerful engine for sustained and healthy economic development. The greatest potential for expanding domestic demand lies in urbanization. According to the latest “National New Urbanization Plan (2014-2020)†data, the urbanization rate of permanent residents in China is currently 53.7%, which is much lower than the average level in developed countries. There is still much room for development. As the urbanization level continues to increase, it will bring about huge investment demand for urban infrastructure, public service facilities, and housing construction. This will provide continuous driving force for economic development and will continue to drive the growth of steel demand. However, we must also see that due to the economic downturn, the growth in steel demand will slow down.

2. Slow growth in demand for steel products, social inventories are still at a high level until the second week of March. The CSPI steel comprehensive price index was 95.43 points, which fell to the lowest point since February 2006. As the market expects the steel price to basically fall to the bottom, under the influence of the expected increase in the market outlook, the steel society stocks will increase rapidly. At the end of February, the five major steel stocks in major markets across the country totaled 20.86 million tons, up 5.27 million tons month-on-month, or an increase of 33.76%, an increase of 18.31 percentage points from the previous month. However, from the situation in March, due to the lower than expected growth in demand for steel products, stocks have shown a downward trend. Due to the rapid growth in the previous period, the reduction of inventory in the later period will put pressure on the trend of steel prices.

3. The prices of raw materials still have room to fall. Steel prices are facing downward pressure. According to data from iron ore price monitoring systems of the Iron and Steel Association CIOPI, as of March 17, the price of imported iron ore fell to US$107.89/ton, which is A trading day rose; coking coal prices have shown a steady upward trend recently. During the same period, the CSPI steel price index was 95.43 points and continued to fall. Compared with steel prices, there is still room for further decline in raw material prices, and steel prices are facing downward pressure.

The main issues that the market needs to pay attention to in the later period:

The first is that steel production maintains a high level, which is not conducive to the rebound of steel prices. In the first two months of this year, the level of crude steel production reached 2.217 million tons, a record high. With the slowdown in demand for steel, the output of steel still maintains a relatively rapid growth. The contradiction between supply and demand in the market is further aggravated and it is not conducive to a rebound in steel prices.

The second is that steel prices continue to operate at a low level, which is detrimental to the efficiency of enterprises. As of March 14, the comprehensive price index of the steel association CSPI steel fell to 95.43 points, the lowest level since March 2006. The decrease in production costs of enterprises is far lower than steel prices, and steel prices continue to operate at a low level, which is detrimental to the improvement of economic efficiency of enterprises.

Third, the increase in international trade friction, and the difficulty in the export of steel products in the later period. Following the European Union's investigation of the suspected dumping of cold-rolled stainless steel plates produced in China, the United States also launched an anti-dumping and anti-subsidy merger investigation on carbon and alloy steel wire rods imported from China. With the increase in trade frictions in the steel industry, steel companies have become more difficult to export steel products.